Stephen’s story

Retired with $300,000 in super.

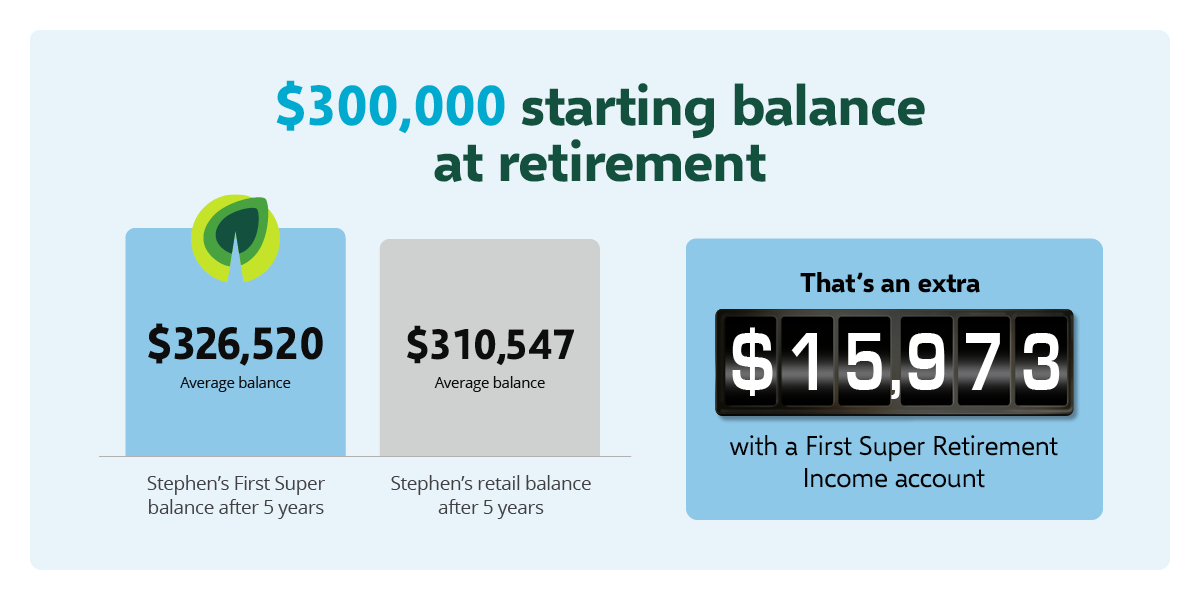

Stephen is 70 and has worked as a mechanic for most of his life and has been getting super for a long time. On his 65th birthday he retired with $300,000 in his super.

Stephen has always planned for his super to be his main source of income in retirement, so he met with one of First Super’s financial planners to discuss his options. The planner suggested he convert his super into Retirement Income account and start drawing down on it gradually while also taking a small amount of the Government Age Pension as a top-up.

This strategy allowed the balance in Stephen’s First Super Retirement Income account to remain invested while he could also still be in control of his balance with the flexibility to choose how much he wanted to take as an income and how often. He could also withdraw extra money anytime he wanted.

Stephen’s balance continued to grow in the early years of retirement while also providing him with an income. And as an added bonus, Stephen was better off than if he had switched to a retail super fund.

Here’s what that looked like:

- Stephen’s super balance was $300,000 when he retired, and he converted it into a First Super Retirement Income account.

- Over the past five years he withdrew on average around $15,068 a year from his Retirement Income account and was also able to access the Government Age Pension to supplement this income.

- Stephen experienced an annualised five-year First Super investment return of 6.95% (2019-2024)1.

- Today, his First Super balance has grown to $326,520.

- If Stephen had switched to a retail fund pension product at retirement, his balance would only be $310,547.

That’s a difference of over $15,973, simply because he stuck with First Super.

Stephen’s numbers

| Account balance invested after income taken | Income stream payments | Age Pension payments | Total income | |

| 2019/20 | $300,000 | $15,000 | $25,928 | $40,928 |

| 2020/21 | $281,512 | $14,076 | $27,858 | $41,934 |

| 2021/22 | $312,051 | $15,603 | $27,796 | $43,399 |

| 2022/23 | $299,894 | $14,995 | $29,129 | $44,123 |

| 2023/24 | $313,358 | $15,668 | $31,482 | $47,150 |

| Closing balance | $326,520 |

We’re here to help. So, let’s talk

If you have any questions, call our Member Services team on 1300 360 988, email us or use the Live Chat. The 5% drawdown may not be right for you, so book an appointment with one of our financial planners to discuss your situation or click the link below to find out more about our Retirement Income account.

Stephen is not an actual member. His story has been created for illustrative purposes.

1Past performance is not a reliable indicator of future performance and should never be the sole factor considered when selecting a fund. Investment return figure follows SuperRatings’ Net Benefit Modelling (including the returns after fees are taken out) applied to all Industry SuperFunds’ performance figures, which is different from First Super’s 7.01% calculated return for the same period.

Comparisons modelled by SuperRatings, commissioned by ISA and show average difference of the ‘main pension Balanced option’ of First Super and retail funds tracked by SuperRatings, over a 5 year period. A ‘main pension Balanced option’ being the fund’s largest pension Balanced option where 60% to 76% of the fund’s assets are invested in growth investments. Where a fund does not have a Balanced option, the option closest to SuperRatings’ benchmark range of 60% to 76% growth investments is used. Outcomes vary between individual funds. Modelling performed on 16 October 2024 using data as at 30 June 2024. See firstsuper.com.au/retirement-assumptions for more details about modelling calculations and assumptions.

First Super financial planners are authorised representatives of Industry Fund Services Limited (ABN 54 007 016195, AFSL 232514).

Issued by First Super Pty Ltd (ABN 42 053 498 472, AFSL 223988), as Trustee of First Super (ABN 56 286 625 181). This article contains general advice which has been prepared without taking into account your objectives, financial situation or needs. You should consider whether the advice is appropriate for you. Read the Product Disclosure Statement (PDS) before making any investment decisions. To obtain a copy of the PDS or Target Market Determination please contact First Super on 1300 360 988 or visit our PDS & Publications page.